Following high-profile increases in activism and protests against climate change, Simon Cadbury asks what more retail banks can do to address the issue and become more eco-friendly in their operations

While the Extinction Rebellion protesters were recently gluing themselves to the London Stock Exchange and storming the Barclays AGM, they found an unlikely ally in Mark Carney.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

At the same time, the governor of the Bank of England, alongside other central bank leaders, signed an open letter outlining an intention to place more scrutiny on those under their jurisdiction.

The letter stated: “No country or community is immune. As financial policymakers and prudential advisors, we cannot ignore the obvious risk before our eyes.”

It was part of a more long-standing effort to get banks to treat climate change as a risk, rather than just as a box-ticking environmental, social and governance issue.

So, how are retail banks addressing the issue currently? Within the realms of investment banking, steps have been taken to help consumers make informed choices. For example, stocks can now be screened on environmental, social and governance (ESG) criteria, and we have seen ethical funds (+76.1%) outperform non-ethical funds (+64.1%) over the last five years.

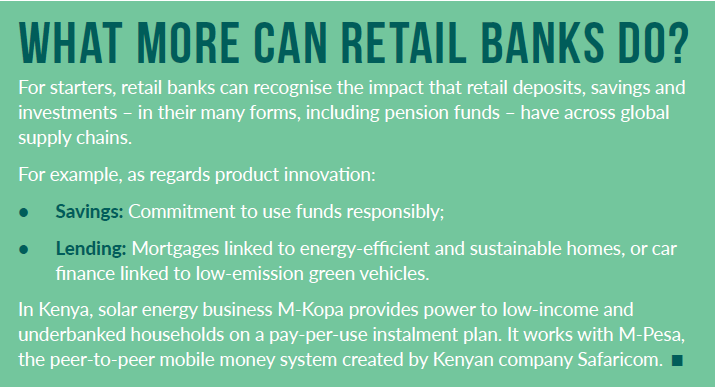

However, with the exception of rather meek attempts to ask consumers to switch to paperless statements, we have yet to see mainstream retail banks create meaningful propositions to help address the ‘climate emergency’.

Compelling evidence from other industries has demonstrated that helping the planet can also be good for business. Bulb, a provider of 100% carbon-neutral energy, has lured 1.2 million customers away from the ‘big six’ in just three years. Meantime, Marks and Spencer has received more than 2 8 million garments donated to its stores since it started offering vouchers for recycling.

However, if Extinction Rebellion founder Gail Bradbrook gets her way, there will be a “mass refusal” to pay off loans and mortgages in a bid to drive greater action.

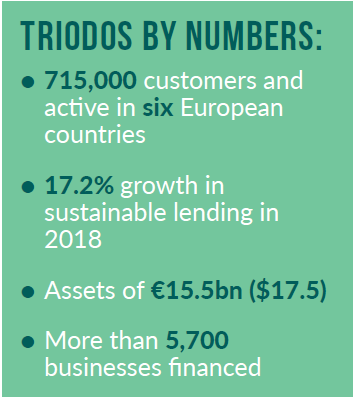

Retail banks could take a leaf from Triodos. Its mission is to offer sustainable financial products which enable “individuals and organisations to use their money in ways that benefit people and the environment”.

Also ahead of the game is Australia’s UBank. Funds deposited into Ubank’s green term account are matched to a portfolio of renewable energy projects such as solar and wind power, and low-carbon transport and buildings.

Opportunity for banks

There is a real opportunity for retail banks, given their detailed understanding of customer spending habits. They also enjoy a captive audience in online and mobile banking.

They can leverage their unique position to help consumers better understand the impact of their behaviour, and nudge them to make alternative choices. There are three facets to such a proposition:

1. Rate: Provision of a ‘score’ within online and mobile banking, based on an individual’s purchases – flights, fuel or utility bills, for example – and providing an estimate of the carbon consumed;

2. Compare: Using this data to enable an individual to compete with peer groups – be they friends and family or a wider demographic, and

3. Reward: Offering carbon-offset mechanisms such as ‘points’ which are provided for responsible purchases or improvements in the ‘score’, and can then be donated to green initiatives such as planting a tree, or even pooled with friends to contribute to a community cause, such as a solar panel for the village hall.

Green rewards

Let us give this ideal a working title of Green Rewards – and if you will excuse the pun, the opportunities outlined above are just the tip of the iceberg.

Green Rewards could also offer ties with retailers, utilities, payment service providers and even fitness trackers to extend the data captured and applicability of the approach. For example, a consumer could be provided with incentives to switch to a green energy provider – in the same way that Monzo is trialling the ability to switch through its app – or be rewarded for walking or cycling instead of using a car. Links with outlets such as eBay and the Freecycle network could be established to reward recycling.

The scheme could also be utilised within the realms of business banking, in turn driving a greater understanding of the impact of spend across an even wider part of the supply chain. Such a proposition could be funded by interchange, merchant incentives, monetisation of the data, as well as lower customer-acquisition costs.

Making an impact

Green Rewards would offer a highly differentiated proposition that would drive engagement and discussion, while also encouraging consumers and retailers to share more data to increase both the individual’s and wider society’s understanding of our impact on the environment.

With the rise of digital banking and improved analytics, alongside the opportunities of Open Banking, retail banks have never been in a better position to make a meaningful impact on shifting consumer behaviour and helping to avert the ‘climate emergency’.