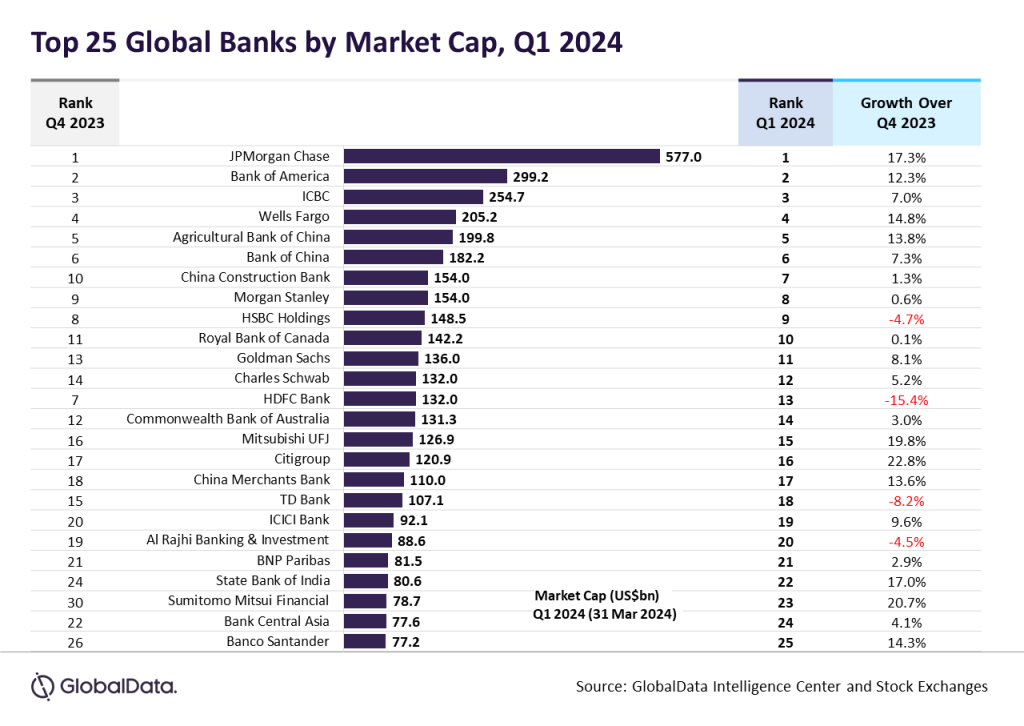

The aggregate market capitalisation (MCap) of the top 25 global banks surged ahead by 7.8% to $3.89trn quarter-on-quarter (QoQ) during the first quarter which ended on 31 March 2024, driven by expectations of interest rate cuts. Notable highlights include Citigroup and Sumitomo Mitsui Financial stocks recording over 20% growth, while HDFC Bank faced a significant decline of over 15% in market value. Despite challenges, JPMorgan Chase retained its position as the most valuable bank for the eighth consecutive quarter, reflecting resilient performance amidst evolving economic landscapes, reveals GlobalData, a leading data and analytics company.

Murthy Grandhi, Company Profiles Analyst at GlobalData, commented: “Investor optimism surged on the Federal Reserve’s hint of potential interest rate cuts in 2024, coupled with easing inflationary pressures. Economic resilience, highlighted by a 2.5% real GDP growth in 2023 and a projected 2.1% for 2024, diminished recession concerns. With inflation nearing the Fed’s 2% target, prospects for a soft landing for the US economy are favourable. These trends buoyed investor confidence, supporting bullish sentiment towards bank stocks amidst stable deposit costs and robust lending environments.”

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

JPMorgan Chase continues to top for the eighth consecutive quarter

Citigroup’s stock value surged by 22.8% following its comprehensive reorganisation, which involves streamlining its structure into five core businesses. The bank is actively tackling issues highlighted by regulators in enforcement actions known as consent orders since October 2020. Citigroup is prioritising enhancements in data governance, risk management, controls, and automation, contributing to the positive trajectory of its stock price.

Sumitomo Mitsui Financial Group experienced a significant 20.7% surge in its market capitalisation, reaching $78.7bn by 31 March 2024. This growth was propelled by the bank’s expansion efforts in the APAC region and Bank of Japan’s decision to eliminate its negative interest rates policy.

Grandhi continues: “In Q4 2023, JPMorgan Chase strengthened its position as the top bank, achieving a 12% increase in revenue to $39.9bn compared to the same period in 2022. This growth was predominantly fueled by elevated rates and revolving balances in Card Services, although it was somewhat offset by reduced deposit balances.”

HDFC Bank experienced a 15.4% fall in its market capitalisation to $132bn from the previous quarter. The decline was mainly linked to merger-related challenges, increased operating costs, and reduced yields due to higher home loan volumes at HDFC Ltd.

The market value of China’s top four banks, ICBC, Bank of China, Agricultural Bank of China, and China Construction Bank, experienced growth in the range of 1%-13%.

Grandhi adds: “All these banks experienced a decline in net interest margins for the fiscal year ending in December 2023 due to factors including a reduction in the loan prime rate, shifts in deposit maturity structures, a decrease in the average yield of interest-earning assets, ongoing repricing of existing assets such as residential mortgage loans, and a rise in the average cost of interest-bearing liabilities influenced by market conditions.”

GlobalData predicts the banking industry to face challenges in 2024 due to a slowing global economy and a divergent economic landscape. Banks may continue to face challenges in generating income and managing costs amidst disruptive forces challenging the industry’s basic tenets. The key drivers of this transformation include reduced money supply, more stringent regulations, climate change, and geopolitical tensions.

Grandhi concludes: “The banking industry is set to undergo significant transformations in 2024 driven by a rapid influx of new technologies and a convergence of various trends. These changes are reshaping how banks function and cater to customer requirements. The impact of generative AI, industry convergence, embedded finance, open data, digitisation of money, decarbonisation, digital identity, and fraud is expected to intensify throughout the year, influencing the operations and strategies of financial institutions.”