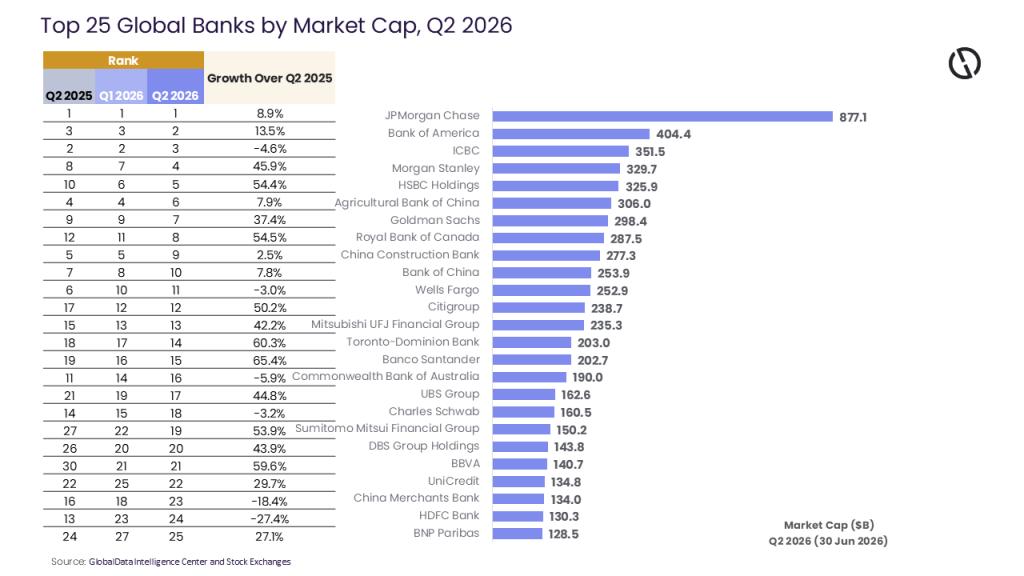

The global banking sector delivered a markedly different market-cap ranking by the end of the second quarter of 2026 (Q2), as investors rewarded banks that combined resilient earnings, generous capital returns, and stronger investment banking activity.

While the largest US banks retained their dominance, European lenders emerged as some of the biggest winners, Japanese banks continued to benefit from changing domestic interest-rate dynamics, and several Chinese banks lost relative ground amid persistent concerns over the country’s economic outlook, according to GlobalData, publishers of RBI.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

JPMorgan Chase remains a solid #1

JPMorgan Chase comfortably retained its position as the world’s most valuable bank, with its market capitalisation up 8.9% year-on-year (y-o-y). The rise reflects investor confidence in its diversified model, industry-leading profitability, strong consumer franchise, and consistent fee generation across investment banking, payments, and wealth management. Disciplined capital allocation has further supported its valuation.

Murthy Grandhi, Company Profiles Analyst at GlobalData, said: “US dealmakers and wealth managers saw a surge in their valuations in the second quarter. Morgan Stanley jumped from eighth to fourth (+45.9%) as its transformed business mix paid off. Wealth management posted record revenue as higher asset values and a revived IPO and M&A pipeline—with first-half 2026 global equity issuance exceeded $250bn—lifted fee and advisory income, with advisory revenue rising sharply on completed deals.”

Goldman Sachs (+37.4%) benefited from the same capital-markets reopening after the 2024–25 “M&A winter.” Citigroup rose 50.2% as Jane Fraser’s restructuring improved efficiency and enabled buybacks, while Bank of America gained 13.5% on stable net interest income and trading strength.

By contrast, ICBC slipped to third after a 4.6% decline amid weaker Chinese credit demand, property stress, tighter margins from rate cuts, and concerns over local government financing vehicles.

HSBC market cap soars by +54%

HSBC was the standout: up 54.4% to fifth globally, driven by CEO Georges Elhedery’s overhaul, record pretax profit, strong Hong Kong/Asia wealth, and higher-for-longer rates boosting margins on its large deposit base. Royal Bank of Canada and TD Bank also advanced on resilient North American lending and wealth platforms.

Grandhi added: “Europe saw the strongest valuation expansion: Santander +65.4%, BBVA +59.6%, UniCredit +29.7%, and BNP Paribas +27.1%. Higher rates lifted net interest income, while cost discipline, stronger capital, and dividends/buybacks boosted confidence. Consolidation talk, and rotation from pricey US tech into cheaper European value amplified gains.”

Japanese banking groups also attracted renewed investor interest. Mitsubishi UFJ Financial Group rose 42.2%, while Sumitomo Mitsui Financial Group gained 53.9%. The gradual normalisation of monetary policy by the Bank of Japan has improved long-term earnings prospects by supporting wider lending margins after decades of ultra-low interest rates.

Not every bank participated in the rally. Commonwealth Bank of Australia fell 5.9% as Australia’s slowing credit growth and increasing mortgage competition moderated earnings expectations despite the bank’s premium franchise. Charles Schwab declined 3.2% as investors remained attentive to deposit mix normalisation following industry-wide funding shifts.

HDFC Bank market cap -27%

HDFC Bank, India’s largest private lender, was down 27.4% after being hit by a governance shock: chairman Atanu Chakraborty’s resignation in March, citing unspecified ethical concerns, wiped out millions in market value within three trading sessions. That coincided with a multi-crore internal vigilance probe, sustained foreign institutional outflows, and a weakening rupee — all compounded by the broader risk-off mood from the Iran conflict and elevated crude prices.

Grandhi concluded: “Looking ahead, GlobalData anticipates that the outlook depends on three swing factors: the Fed’s rate path amid inflation risks from Middle East-driven energy prices; China’s success in stabilising property and consumer credit; and whether Europe’s bank re-rating shifts from capital returns to real loan growth. US investment banks may benefit if IPOs (OpenAI, Anthropic, and others reportedly weighing listings) and M&A stay strong. Rate cuts could temper Europe’s earnings. Japan stands to gain as rates normalise. China remains constrained pending a clearer recovery.”