Customers are increasingly open to switching their business to non-financial services outfits in general, and the ‘BigTech’ players in particular, according to the 2018 World Retail Banking Report. Douglas Blakey reports

Customer expectations continue to soar, and the threat from nontraditional competition is rising.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

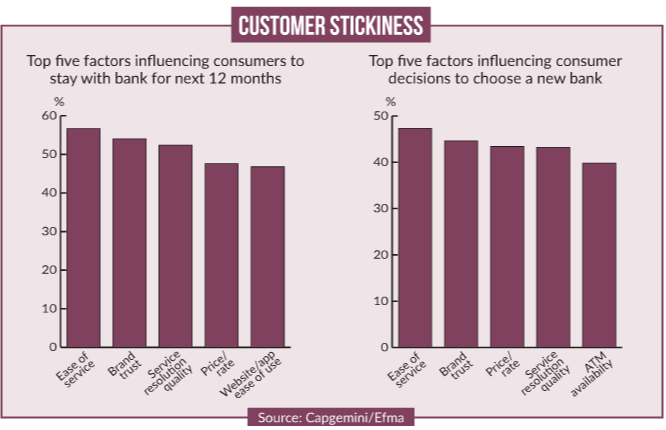

Consumers are increasingly willing to switch to BigTech alternatives, according to the 2018 World Retail Banking Report. Retail banks need to collaborate with the competition and personalise customer experience, or face the consequences.

Key takeaways from the report include: Satisfaction is low: Barely half of customers say their experience across different bank channels was positive (51.1% in branch, 46.9% on mobile and 51.7% on internet banking), despite continued bank investment.

The BigTech threat: nearly a third of customers (32.3%) might consider BigTechs for financial products and services – that includes 43% of Gen Y respondents, 53% of tech-savvy consumers and 70.2% of those already likely to switch their primary provider.

Personalisation is key

Satisfaction was notably higher among those customers who had been offered personalised digital experiences proactively (49.1%) than those who had not (39.5%).

The report, published by Capgemini and Efma, also surveyed banking executives about the main causes of industry disruption. The most-cited factor was rising customer expectations, with nearly three out of four executives (70.8%) stating that positive experiences in other sectors mean customers now expect more from their banking provider.

A majority of executives (58.3%) also said regulatory pressure was a cause of disruption, while 54.2% identified the increasing demand for digital channels as a factor. As lines between traditionally different industries start to blur, banks now face increasing competition from non-traditional firms targeting niche areas of the banking value chain.

Also, increasing digitisation and the explosion of new technologies are rapidly changing the banks’ ways of working.

“With fintechs, BigTechs and other non- FS firms finding their place in the market, retail banking today is all about the customer experience when interacting with their financial institution,” says Anirban Bose, CEO of Capgemini’s financial services strategic business unit.

“As a new, open ecosystem – composed of customers, traditional banks, non-traditional firms, regulators, and developers – takes shape, there is now a clear opportunity for banks to leverage digital transformation to retain customer relationships by reinventing the customer journey and creating new revenue streams.”

Despite the reality of growing regulation, non-traditional competition, emerging technologies and customer expectations, banks are not powerless to use change to their advantage.

A significant majority of banking executives (70.8%) think they can ‘generate non-traditional revenue’ via collaboration with fintech and BigTech providers, whether to develop a new service or distribute third-party products via a marketplace platform.

Most banks believe there are untapped opportunities to make more strategic use of data to improve the customer experience: executives said they plan to use customer data to create smoother customer journeys (87.5%), develop relationship-based pricing (75%), build personalised loyalty rewards (58.3%) and create lifecycle-stage products and services (54.2%).

“The retail banking industry is at an inflection point and needs to determine its role going forward in the open banking ecosystem. There is opportunity to innovate through collaboration as well as reinvention,” says Efma secretary general Vincent Bastid.

“It is an exciting time to be in banking as regulation, innovation, competition and collaboration merge to form the bank of the future.” This years report features data from more than 10,000 retail banking customers in 20 countries, and interviews with 60 senior banking executives across 23 markets.