Synovus Q2 2019 net income for the quarter to end June of $153m is up by 40% year-on-year and beats analyst forecasts.

Second quarter highlights include period-end loan growth of $504m or 5.7% annualised from the prior quarter.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Synovus also reports steady growth in commercial and industrial loans.

Average non-interest-bearing deposits rise by 15.1% sequentially.

Key credit metrics continue to improve, with non-performing asset and non-performing loan ratios declining 5 and 6 basis points, respectively.

“Our results reflect the strength of our core business and geography,” says Kessel D Stelling, Synovus chairman and CEO.

In particular, Stelling flags up Synovus’ broad-based loan growth, solid credit and profitability metrics.

“We are pleased with the early wins in our expanded Florida footprint as we introduce our broader capabilities to new customers and prospects. We not only expect continued successes in that region, but across our entire footprint.”

Synovus Q2 2019: other highlights

Other notable highlights include a 285 basis point drop in the cost-income ratio to 54.14%.

Capital ratios remain strong and all increased slightly during the second quarter.

Less positive metrics include the bank’s net interest margin.

Margin pressure results in a 17 basis point drop y-o-y in the Synovus net interest margin to 3.69%. There is also a slight increase in provisions for loan losses to $12.1m from $11.8m a year ago.

Synovus operates 297 branches in Georgia, Alabama, South Carolina, Florida, and Tennessee.

Last July, Synovus announced the acquisition of $12bn assets, 51-branch strong Florida Community Bank. That deal closed this January. As a result of the acquisition, Synovus became a top five regional bank by deposits in the Southeast of America.

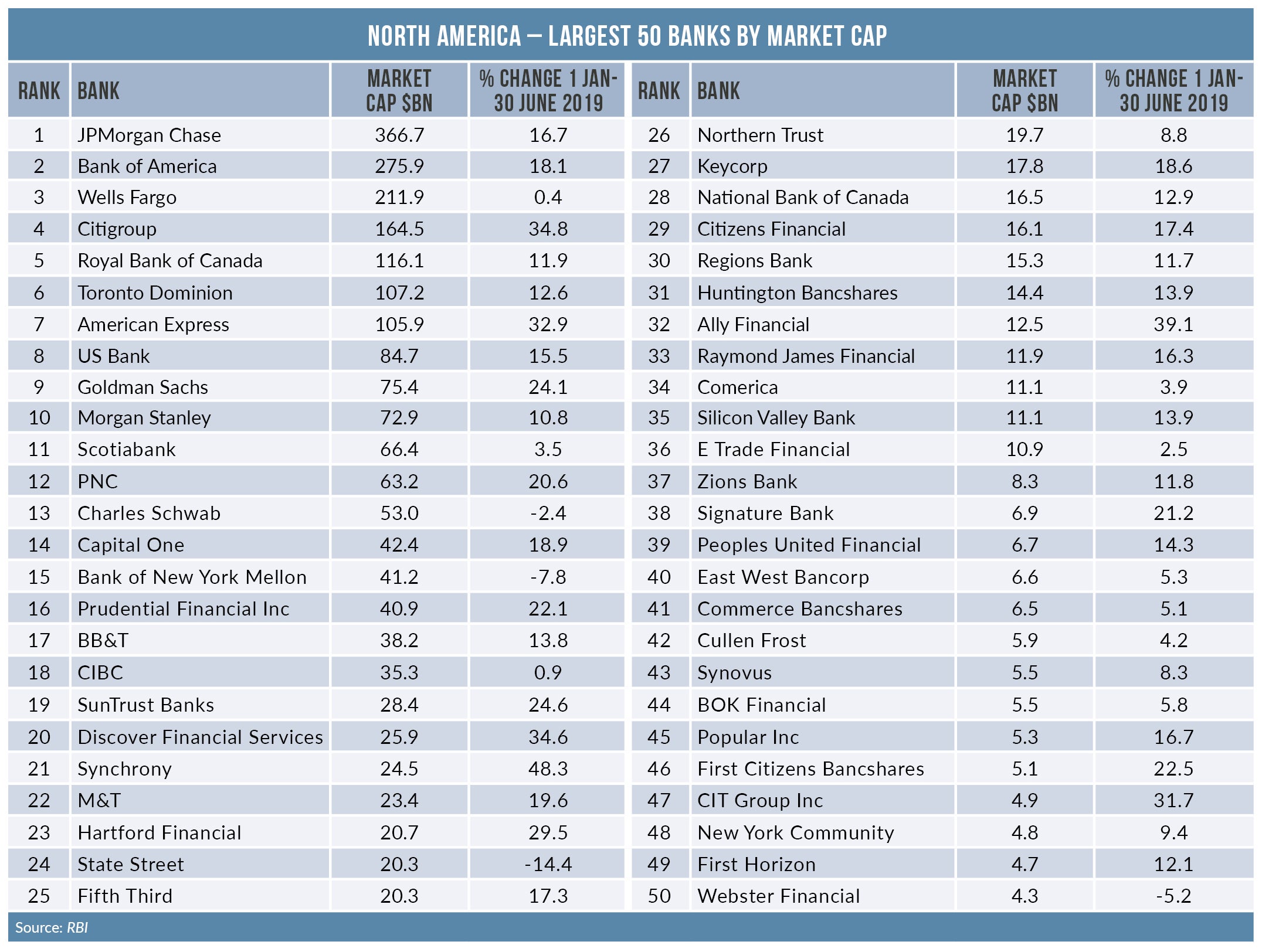

The Synovus share price is ahead in the first half but only up a relatively modest 8%. This compares to a sector average of almost 20% in the period 1 January to 30 June (see table).