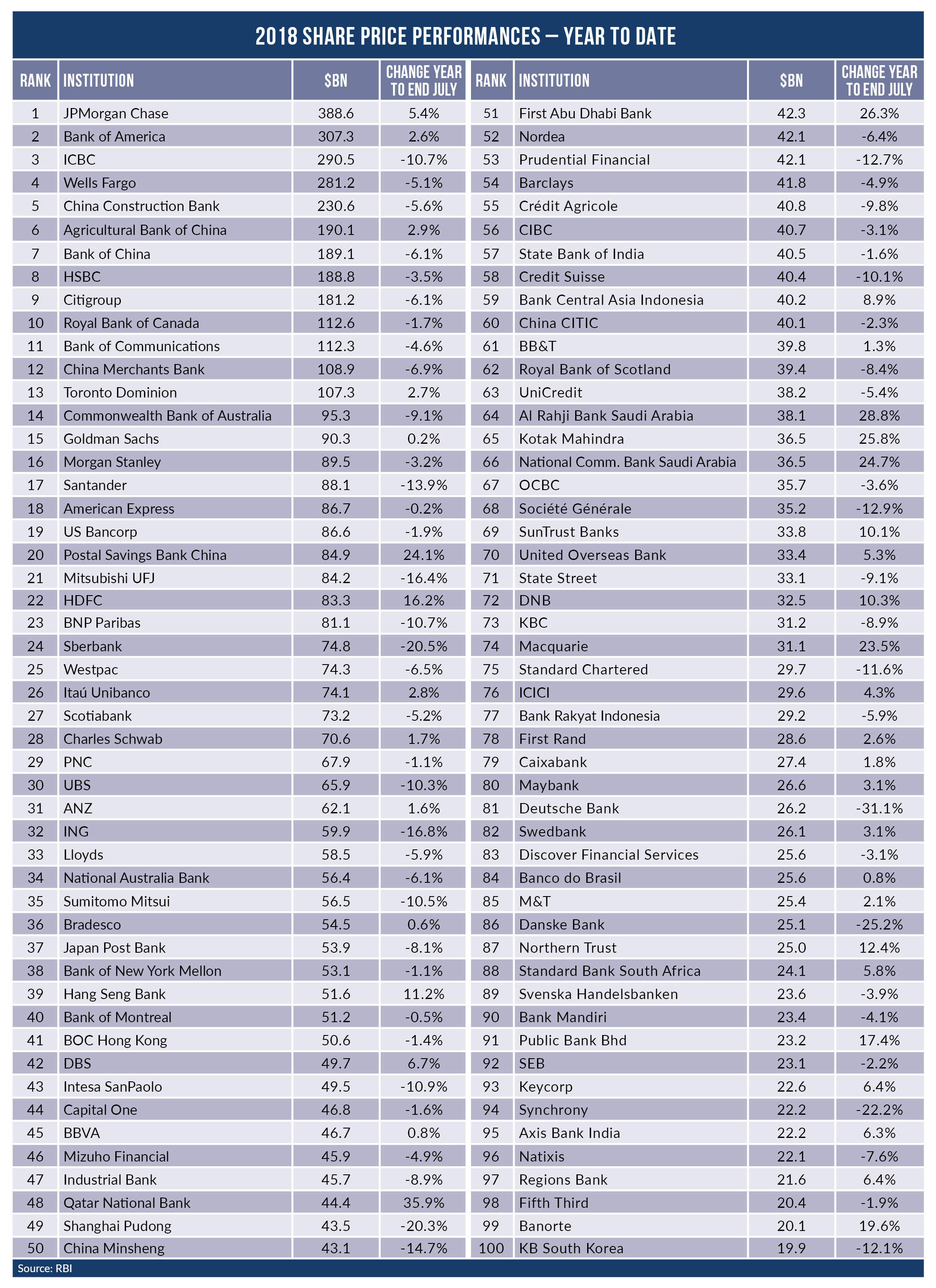

Only six of the 20 biggest banks in the world are showing a share price gain for the year to end July. 2018 is not shaping to be a memorable year for the majority of bank shareholders despite some positive news regarding dividends, writes Douglas Blakey

With one or two notable exceptions, share price gains have been modest in 2018.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

JPMorgan Chase remains by far the largest bank by market cap and its Q2 earnings once again beat analyst forecasts.

Chase posted a record second quarter net income of $8.32bn, up 18.5% from the year ago quarter.

Of particular note is Chase ongoing success in growing its digital proposition.

Active digital banking customers rose by 4.5% to 47.95 million. Chase mobile banking customers rose by 10.4% to 31.65 million.

The top 10 biggest banks by market cap remain unchanged with 4 US lenders and 4 from China.

UK headquartered HSBC and Royal Bank of Canada round off the top 10.

Of the top 20, only Postal Savings Bank China can boast a double digit share price gain for the year to date.

Biggest banks in the world: 2018 share price winners

The strongest regional performances are to be found in the GCC banking sector.

Qatar National Bank’s share price is up by more than one third, to rank in the top 50 by market cap for the first time.

First Abu Dhabi Bank’s share price is up by more than 25% for the year to end July. Saudi Arabia headquartered Al Rahji and National Commercial Bank are enjoying similar share price gains.

Emirates NBD is just outside the 100 biggest banks by market cap and is ahead by 28% for the period.

Emirates NBD has enjoyed a strong first half, posting a half-yearly net profit in excess of AED5bn for the first time.

Improved margins, loan growth, a lower cost of risk and digital investment is paying off for Emirates NBD. It is also being reflected in the Emirates NBD share price.

Macquarie: bucking the trend in Australia

To say that 2018 has been a challenging year for Australian lenders is being kind.

CBA, NAB and Westpac are all posting share price losses with ANZ flat for the year to date.

The country’s fees-for-no-service scandal refuses to go away. The biggest Australian retail lenders have had to replay A$250m to customers for whom they failed to provide services.

According to the Australian Securities and Investments Commission, the final fees refunds total could grow to as much as A$850m.

By contrast, Macquarie’s share price is up by almost 25% for the year to end July.

In the second quarter, the Macquarrie share price hit its all time of AS127. Relative to book value, Macquarie’s market cap is at its highest since before the banking crisis.

The biggest banks: UK dividends but no share price recovery

The UK taxpayer will receive a dividend of £149m courtesy of its 62.3% majority stake in Royal Bank of Scotland. Such news is noteworthy and any mention of an RBS dividend something of a novelty.

RBS has not paid any dividend since the days of Sir, now Mr Fred Goodwin.

Pre-crisis, RBS ranked in the top 10 biggest banks in the world by market cap.

At the end of 2006 for example, RBS’ market cap was around $110bn, just ahead of Wells Fargo and a mere $40bn behind Chase.

By way of further contrast, the RBS market cap was more than twice that of Royal Bank of Canada.

Upon release of RBS’ second quarter earnings, CEO Ross McEwan said: “The turnaround of the bank is almost complete.”

Such optimism is not yet reflected in its share price with RBS down 8% for the year to date. By market cap, RBS remains some way outside the top 50 biggest banks.

Rival Barclays was a regular feature of the top 20 pre-crisis but as with RBS, remains outside the top 50.

Barclays has however enjoyed a strong second quarter, posting a £1.9bn pre-tax profit, up from £659m a year ago.

Operating costs were down and impairments reduced sharply. A positive set of earnings means that Barclays will pay an interim dividend of 2.5p and aims to double the full year dividend to 6.5p.

Meantime, Lloyds improved earnings resulted in an increased interim dividend to 1.07p. Despite all of the positives in the reporting season, Lloyds, Barclays and RBS all show share price losses for the year to date.

The biggest banks: other losers

The well documented ongoing challenges at Deutsche Bank and Commerzbank are reflected in their share price. Pre-crisis, Deutsche Bank’s market cap peaked at more than $60bn. Deutsche ranked about the world’s 25th biggest bank by market cap only a decade ago.

For the year to date, Deutsche Bank’s share price is down by 31% and it now ranks 81st in the top 100. Rival Commerzbank no longer features in the top 100 and is enduring another challenging year. For the year to date, Commerzbank shares are down by 26% with a resultant market cap of only $13b.1bn.

There are however signs of green shoots with Commerzbank Q2 earnings ahead of analyst forecasts. Commerzbank also plans to resurrect its dividend as its transformation programme gathers pace.